Ireland’s housing crisis cannot be simply summarized as cyclical market fluctuations, but is a systemic crisis composed of a series of complex problems, including high housing demand, extremely weak housing production capacity, and severe regional development imbalances. There is no quick fix, and the country is likely to face a long and painful adjustment.

1. The Three Dimensions of Systemic Crisis

1) The Historical Dilemma on The Supply Side

Ireland’s housing supply engine is not just shut down; its most critical component has broken down.

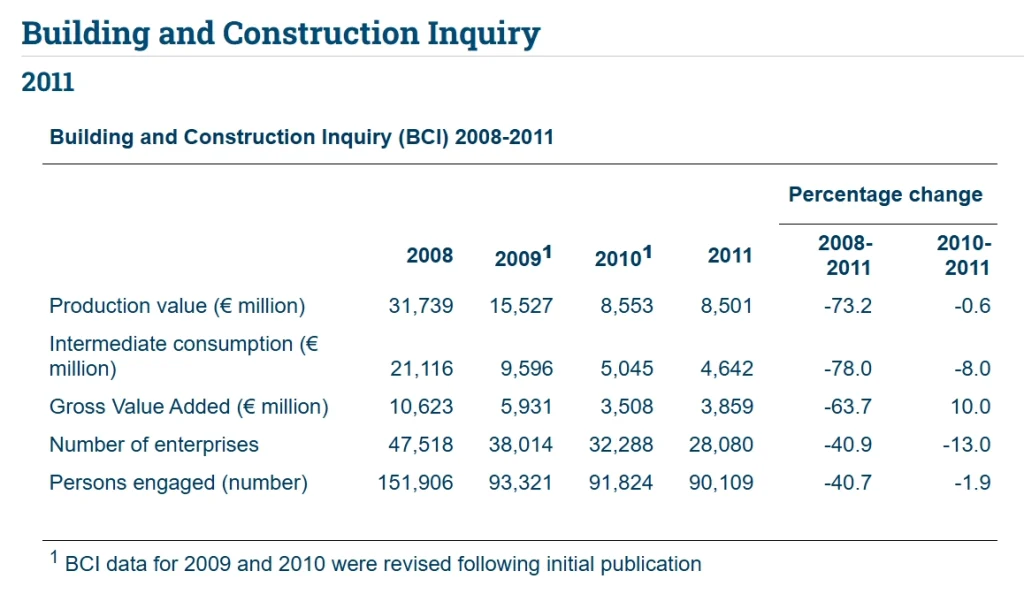

Source: Central Statistics Office

- Historic Disruption and Capacity Loss: The 2008 global financial crisis led to a sudden collapse in Ireland’s construction industry. Between 2008 and 2011 alone, the number of construction firms fell by approximately 40.9%, and around 60,000 workers—about 40.7% of the workforce—exited the industry. This capacity gap cannot be closed quickly. Rebuilding a mature and efficient construction ecosystem requires decades of accumulation.

- Dual Pressures of Cost and Compliance: Today, construction costs are far higher than in the past. High raw material and labor costs, along with stricter building codes, have significantly increased the price of housing. At the same time, the complex planning and approval process increases the uncertainty and time cost of projects, making it more difficult to “rapidly increase supply”.

- The contradiction between profit and demand: In core areas like Dublin, the extremely scarce land supply and high land prices mean that developers can only make substantial profits by building high-end apartments or villas. Meanwhile, the most urgently needed entry-level housing is left undeveloped due to meager profits, and demand is too low in remote areas far from the city center due to inadequate infrastructure and transportation. This is a core contradiction that the market itself cannot resolve.

2) Continued Strong Demand

While supply is extremely difficult, demand is experiencing irreversible and rigid growth.

- Perfect Demographic Structure: Ireland boasts one of the youngest demographic structures in the EU, with a natural birth rate of 10.3%, ranking second in the EU. This means that the home-buying population is large and continues to grow.

- Europe’s Silicon Valley: As a hub for the European headquarters of multinational corporations, Dublin continues to attract top global talent. These individuals possess strong affordability and can easily absorb the limited new housing supply.

- “Safe Haven” Attribute: Ireland’s stable political environment, common law system and English language advantage make its real estate a safe haven asset in the eyes of international capital, which further worsens the home-buying environment for local people with genuine housing needs.

3) The Contradictions of Policy Intervention

The government’s good intentions often create new problems while solving one, thus failing to effectively improve the status quo.

- The Impact of Rent Control: In the short term, this measure protects tenants from the impact of soaring rents, but in the long term, it hurts the incentive of private landlords, causing some landlords to choose to sell their properties. The end result is a decrease in rental housing supply, or the acquisition of properties by capital, leading to higher barriers for tenants.

- The Duality of “Helping to Buy”: The policy aims to help first-time homebuyers raise down payments, but its side effect is that it injects additional purchasing power into the market, which to some extent drives up property prices and increases the cost of homeownership for other buyers.

- Central Bank Cools Down the Market: The Central Bank of Ireland has set strict lending caps to prevent excessive household debt. While this effectively curbed the housing bubble, it also prevented many qualified homebuyers from purchasing property.

2. Why a Short-Term Reversal Is Unlikely

Understanding the systemic nature of the crisis helps explain why a turnaround is not expected in the short term.

- The Time and Talent Gap: Even without planning obstacles and with sufficient funds, it takes at least 2-3 years to build a sizable apartment building. At the same time, although the construction industry has recovered significantly in recent years, it has become segmented into various sub-markets, which is completely unlike the large-scale development prior to the collapse, and it has lost the ability to develop rapidly.

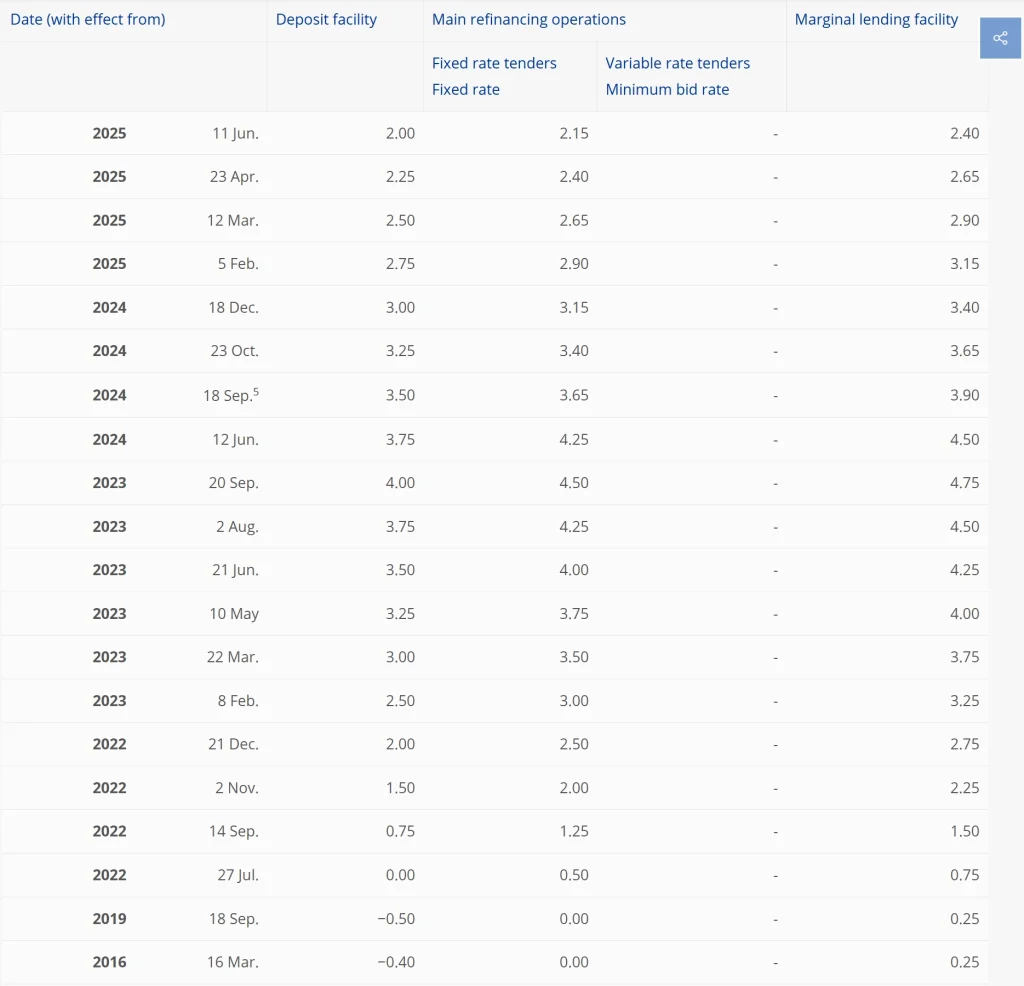

Source: European Central Bank

- Rising Interest Rates Exacerbate the Problem: To combat inflation, the European Central Bank initiated a cycle of sustained interest rate hikes in 2022, causing developers’ financing costs to rise sharply and many new projects to be postponed or canceled, further exacerbating the supply-side situation. Even if rates start to decline in 2025, they will remain high compared to pre-2022 levels.

- Difficulty in Forming a Consensus: Solving the housing crisis requires high-density development in specific areas. However, this is constrained by multiple factors, including land scarcity, vested interests, and obstruction from environmental groups, which makes it difficult to form a broad social and political consensus and renders the project highly uncertain.

3. Future Development

The Irish property market is destined to undergo a slow and painful structural evolution.

- A “dual-track” market: The market will increasingly diverge into two directions. On one hand, there is government-supported affordable housing, serving specific eligible groups. On the other hand, there is a free market where prices are determined by supply and demand.

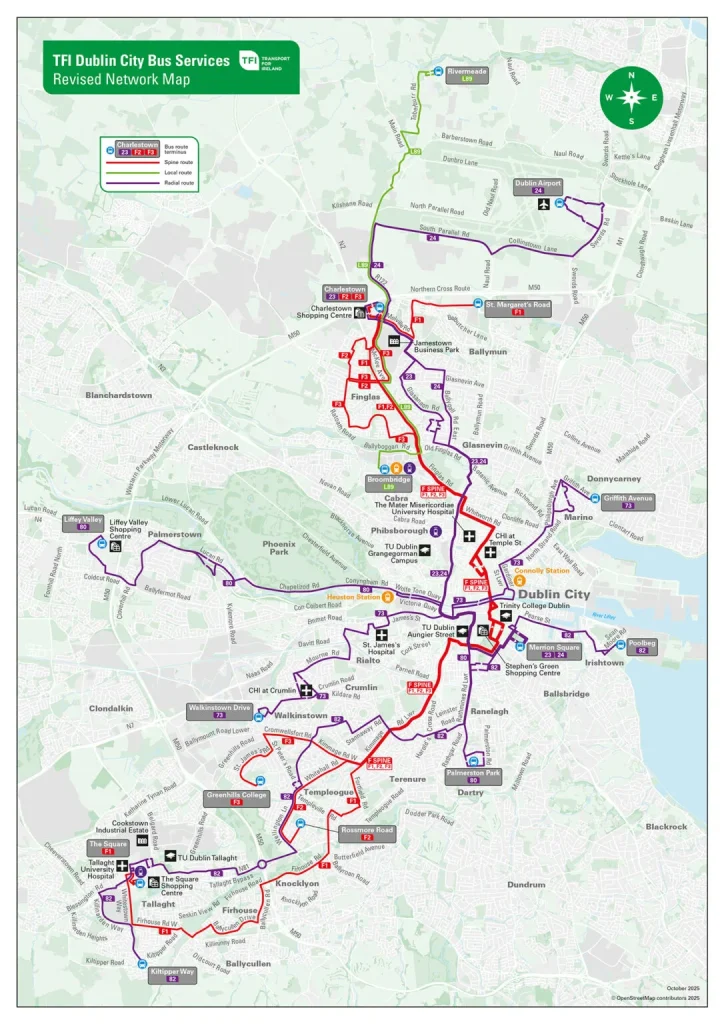

Source: Transport for Ireland

- Reshaping the Geographic Landscape: Dublin is substantially expanding its commuter network through the “BusConnects” public transport system restructuring plan, making a broader metropolitan area possible. Meanwhile, secondary cities such as Cork, Galway, and Limerick are accelerating their development with the support of the national €24 billion transport investment plan, jointly driving the shift of population and economic activity away from Dublin. All of these policies will significantly alleviate Dublin’s housing supply pressure.

- The Shift in Architecture and Residential Culture: In the heart of the city, the traditional “villa with a garden” will give way to high-density apartment living to accommodate more people on limited land. The city skyline will be altered by more high-rise residential buildings, which is a necessary adaptation.

Conclusion: The Ultimate Test of National Resilience

Every country encounters various growing pains during its development. For Ireland, the systemic crisis in the real estate market is an unavoidable growing pain at present. Furthermore, its complexity dictates that a quick resolution is impossible. In the foreseeable future, Ireland will continue to adapt and adjust to this housing crisis, constantly exploring the approach best suited to its circumstances.

Related Reading