When you think of the Philippines, you might feel its tourism can’t compare to Thailand’s, or its economy falls short of Singapore’s. But when it comes to overseas domestic work, I believe the first impression that comes to mind is undoubtedly “Filipina helpers.” However, our focus today is not on domestic helpers, but on the Philippines real estate market—a sector marked by coexisting opportunities and risks, whose complexity is as pronounced as its diversity.

1. Opportunities Driven by Growth Engines

Opportunities in the Philippine real estate market are driven by several solid structural industries.

1) Demographic dividend and Urbanization

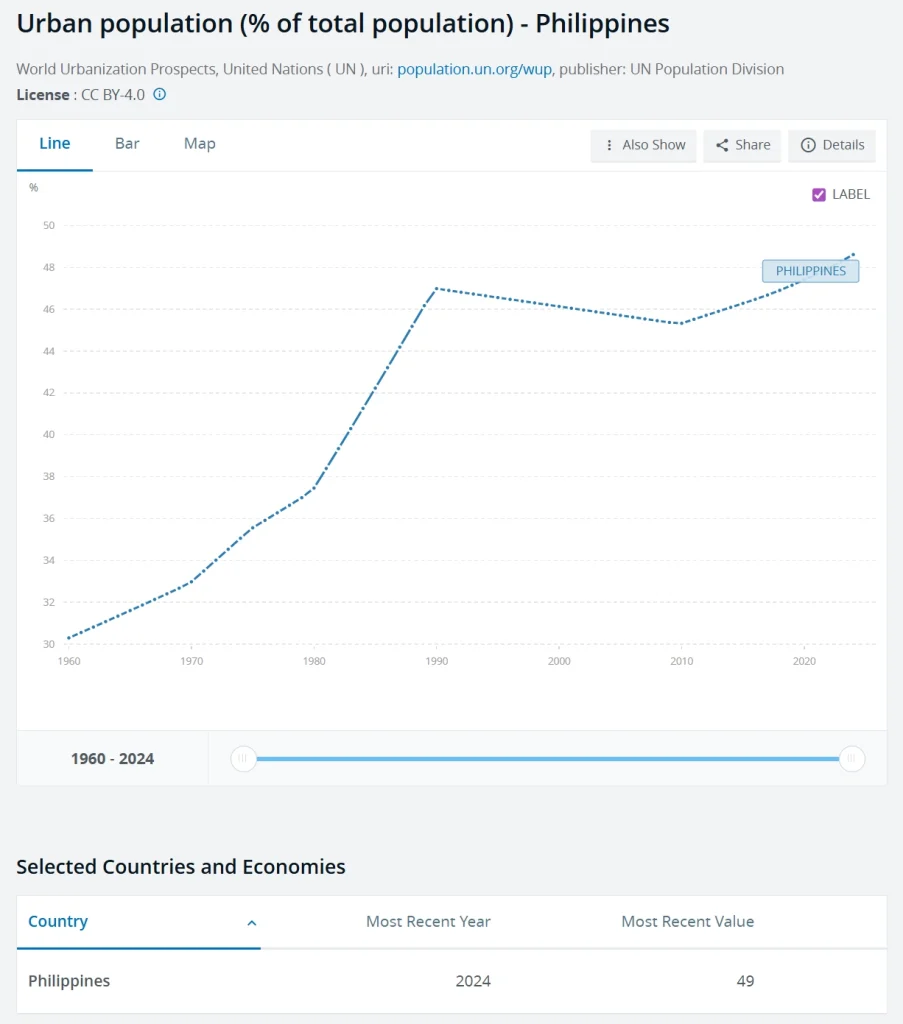

- The Philippines is one of the youngest countries in the world, with a median age of approximately 26.1 years. This means that the country will have a sufficient young workforce and housing demand for the next 20 years. Meanwhile, the urbanization rate in the Philippines is continuing to rise at a relatively rapid pace (reaching 49% in 2024), directly leading to rapid growth in urban real estate. However, rapid urbanization has also led to uneven regional development. For example, Metro Manila, with less than 0.2% of the country’s land area, has nearly a quarter of the country’s population and more than a third of its GDP.

2) Industry Cornerstone – BPO

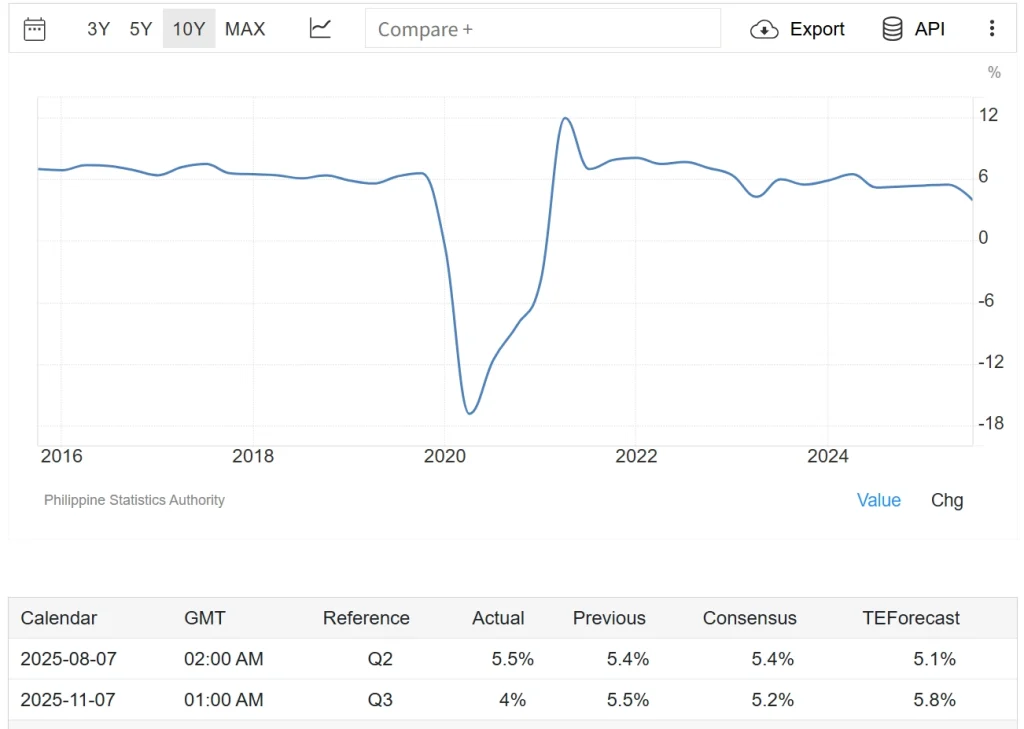

- The Philippine economy has maintained a high growth rate of over 5% for many years, with the business process outsourcing (BPO) industry being the absolute cornerstone of the real estate market. As one of the world’s largest providers of call centers and outsourcing services, the industry employs millions of people with stable incomes, forming the core customer base of the residential rental market and supporting the extremely high demand for office buildings.

3) Stable Remittances from Overseas

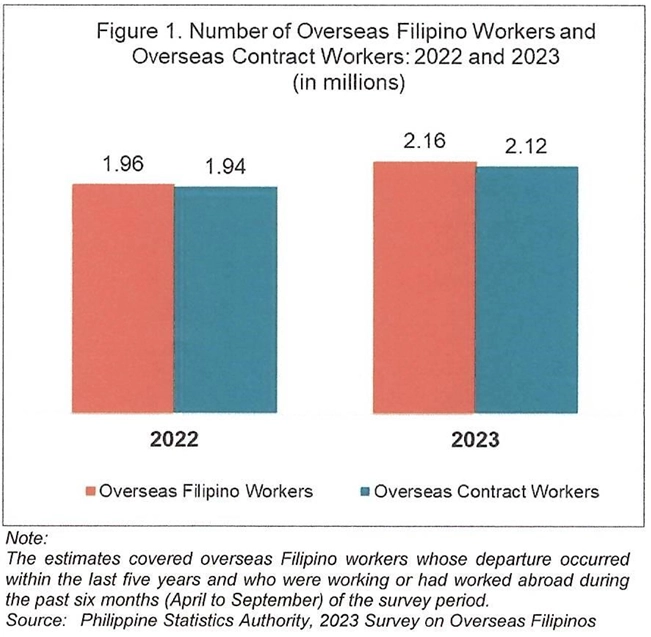

- In 2023, approximately 2.16 million overseas Filipinos remitted 239 billion Philippine pesos (about US$4.06 billion) to the country. This not only created solid domestic demand but also provided support for the real estate market, making it a veritable economic engine for the nation.

4) A Uniquely Advantageous Tourism Industry

- The Philippines’ tourism industry has an inherent advantage, with more than 7,000 islands forming a rich tourism product line, among which Boracay and Cebu are world-class resort paradises. The industry not only attracts a vast number of international tourists who spend in the country, but also drives the robust development of local tourism-related real estate. There is exceptionally strong demand for both short-term rentals and vacation homes.

2. Risks Not to Be Ignored

There are two sides to every coin. Behind every opportunity inevitably lie hidden risks, which must be approached with caution.

1) Ownership Restrictions

The Philippine Constitution clearly stipulates that foreigners cannot own land in the Philippines.

- Freehold ownership: In the Philippines, although foreigners cannot own land, they can legally own freehold units in condominiums, provided that the foreign share in the entire building does not exceed 40%.

- Land lease: For foreigners who want to invest in land and villas, the most common way is long-term lease, usually for 50 years, with the option to renew for 25 years.

2) Inadequate Infrastructure and Traffic Congestion

- This is an inevitable consequence of premature urbanization. The traffic paralysis in Metro Manila is beyond ordinary congestion; it causes billions of dollars in economic losses every year. Although the government has implemented improvement plans, we must recognize that infrastructure cannot be improved in a short period of time. The real problem is that if emerging cities like Cebu and Clark ultimately prove unable to effectively divert population, then Manila’s predicament may not be alleviated.

3) Bureaucratic Problems

- Real estate transactions in the Philippines are often plagued by bureaucratic inefficiencies, including cumbersome procedures, opaque processes, and prolonged processing times. It is quite common for a complete property transaction to take several months, and one may even encounter potential corruption. Even if this problem does not change the long-term value of high-quality assets, it will greatly increase the time and money costs of transactions.

3. Location: The Critical Decision

Core Central Business District

These regions are the engines of the Philippine economy and possess the most resilient assets during market downturns.

1) Makati

- Advantages: This is the Philippines’ undisputed financial center, home to numerous bank headquarters, top firms and financial institutions, as well as top-tier commercial complexes and educational and medical resources. Furthermore, Makati is widely recognized as one of the safest cities in the Philippines. These factors contribute to the area’s strong asset preservation characteristics, while the tenants are of extremely high quality and have stable demand.

- Challenges: The lack of available land has resulted in an extremely limited supply of new homes. With prices already at a premium, this has limited upside potential for capital appreciation. Most critically, Traffic congestion is the biggest problem and is unlikely to improve in the short term.

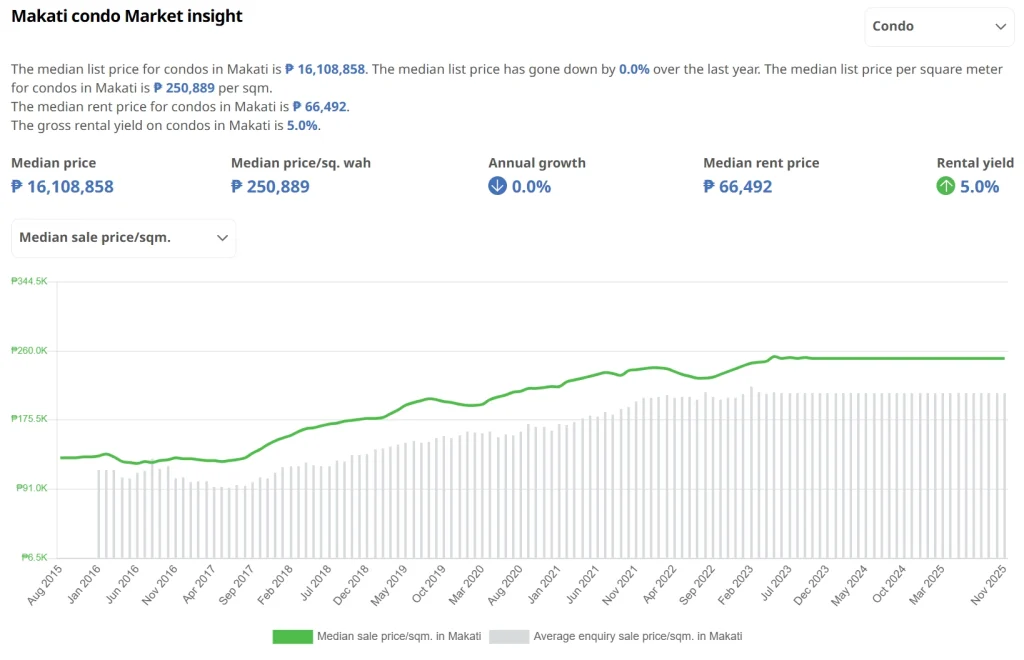

- House Prices and Returns: In 2025, the median listing price for apartments in Makati was 16,108,858 pesos (273,798 USD), the median listing price per square meter was 250,889 pesos (4,263 USD), the median rent was 66,492 pesos (1,130 USD), and the gross rental yield was 5.0%.

2) Bonifacio Global City (BGC)

- Advantages: A well-planned and pedestrian-friendly architectural layout, combined with numerous high-end shopping centers and premium residential areas, has earned it the reputation of the most livable CBD in Manila. It has also attracted the regional headquarters of many top companies (such as Google and Microsoft), enhancing its status as a premier business district. The tenant population here is young, affluent, and international.

- Challenges: Housing and living costs are among the highest in Manila, and external connections are severely congested during peak hours.

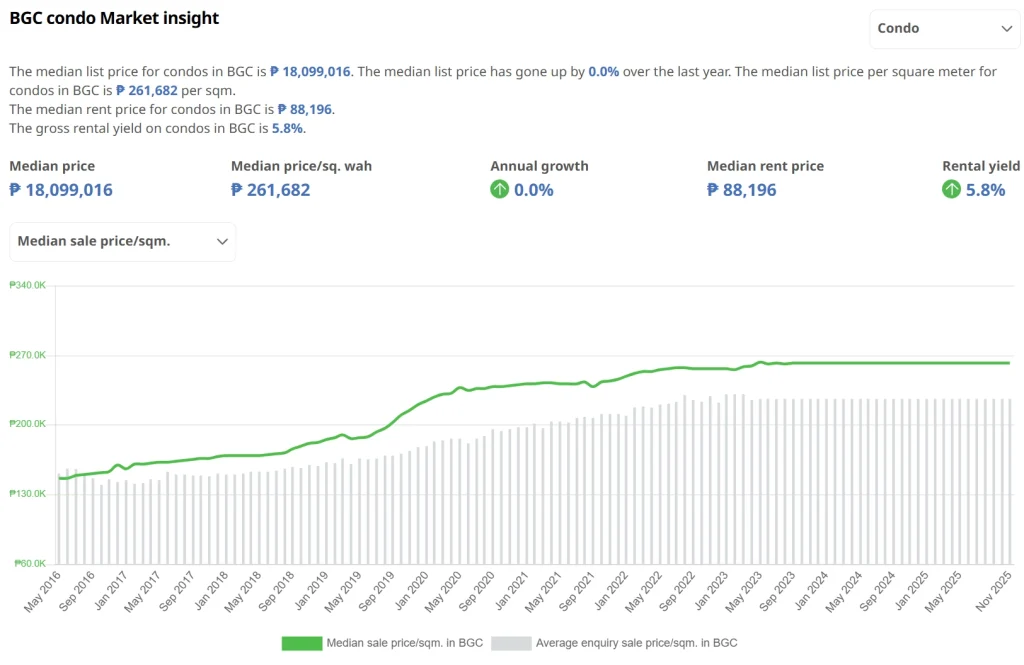

- House Prices and Returns: In 2025, the median listing price for apartments in BGC was 18,099,016 pesos (307,570 USD), the median listing price per square meter was 261,682 pesos (4,447 USD), the median rent was 88,196 pesos (1,498 USD), and the gross rental yield was 5.8%.

3) Ortigas Center

- Advantages: Ortigas is the heartland of the BPO industry and an important educational center, and is one of the regions with the strongest rental demand. Thanks to its large BPO workforce, the vacancy rate has remained low for a long time. Compared to Makati and BGC, house prices and rents here are more affordable, and there are higher cash returns (gross rental yields are generally above 6.5%).

- Challenges: The urban landscape and infrastructure are older than those of BGC, and traffic congestion is very serious. It has not formed a unique advantage compared with other core areas.

4) Manila Bay Area

- Advantages: Manila Bay Area is a future CBD that the government is investing heavily in, representing the future development direction of Manila. Boasting brand-new, forward-looking urban planning and infrastructure, and with a key future transportation hub (Manila Metro Terminal) located here, it is expected to completely transform its accessibility. Currently, housing prices are highly affordable, and the potential for appreciation is enormous. Investing here is equivalent to investing in the future of Manila.

- Challenges: The current living facilities are still incomplete, and it may take 5-10 years for them to fully mature.

Emerging growth centers and tourism hotspots

1) Cebu City

- Advantages: It is the undisputed core of the Cebu metropolitan area, boasting a headquarters economy, high-end commercial facilities, and quality education and medical resources. Meanwhile, Cebu City is the second largest BPO industry hub after Manila, boasting a large and highly skilled young workforce. Compared to the heart of Manila, property prices here are lower, but rental yields are higher.

- Challenges: Due to urbanization, infrastructure and transportation are facing similar problems to those in Manila, and there is no land available.

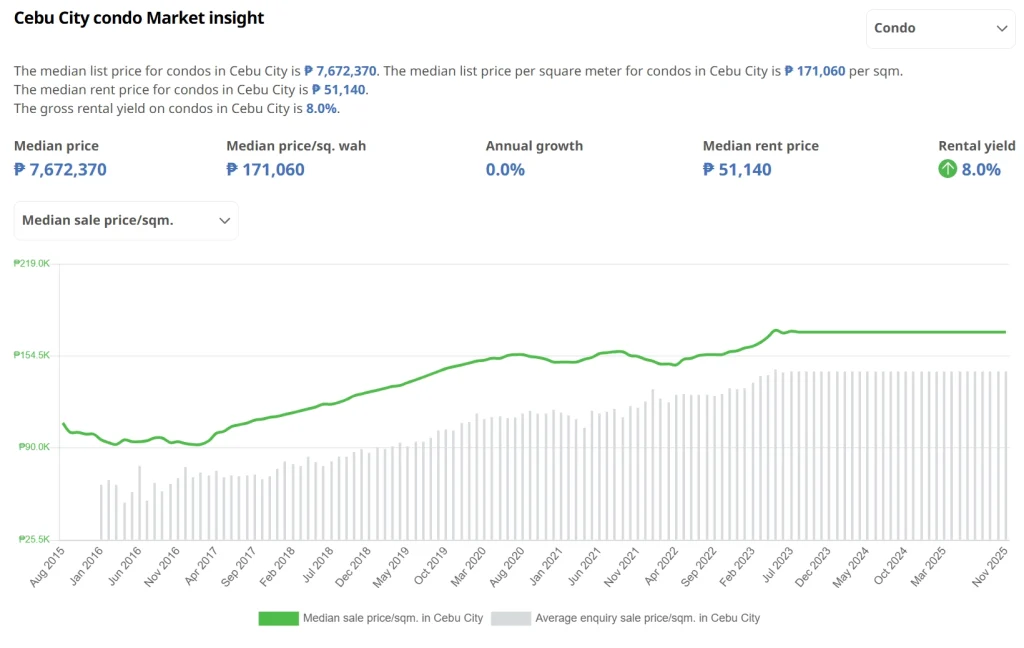

- House Prices and Returns: In 2025, the median listing price for apartments in Cebu City was 7,672,370 pesos (129,900 USD), the median listing price per square meter was 171,060 pesos (2,897 USD), the median rent was 51,140 pesos (866 USD), and the gross rental yield was 8%.

2) Boracay and Palawan

- Advantages: Boasting irreplaceable natural landscape resources, it offers exceptionally high short-term rental yields. Simultaneously, it provides buyers with a vacation home for their own use, achieving a combination of “investment + lifestyle.”

- Challenges: Rental income is highly seasonal and relies on remote property management teams, resulting in high maintenance costs.

- House Prices: In 2025, the median listing price for apartments in Palawan was 5,779,429 pesos (97,890 USD), and the median listing price per square meter was 171,623 pesos (2,906 USD).

Conclusion

Despite the considerable complexity of the Philippine real estate market, with thorough preparation before investing, you can still expect to generate substantial returns in this emerging Southeast Asian market. The key to success lies in making the right decisions at the intersection of opportunity, risk, and location.

Reference Source:

- Philippine housing prices and returns are sourced from Property

- Philippine age data is sourced from World Economics

- Philippine urbanization data is sourced from World Bank Group

- Philippine GDP data is sourced from Trading Economics

- Philippine overseas worker (OFW) data is sourced from Republic of the Philippines

Related Reading