1. Introduction: Concerns Behind Growth

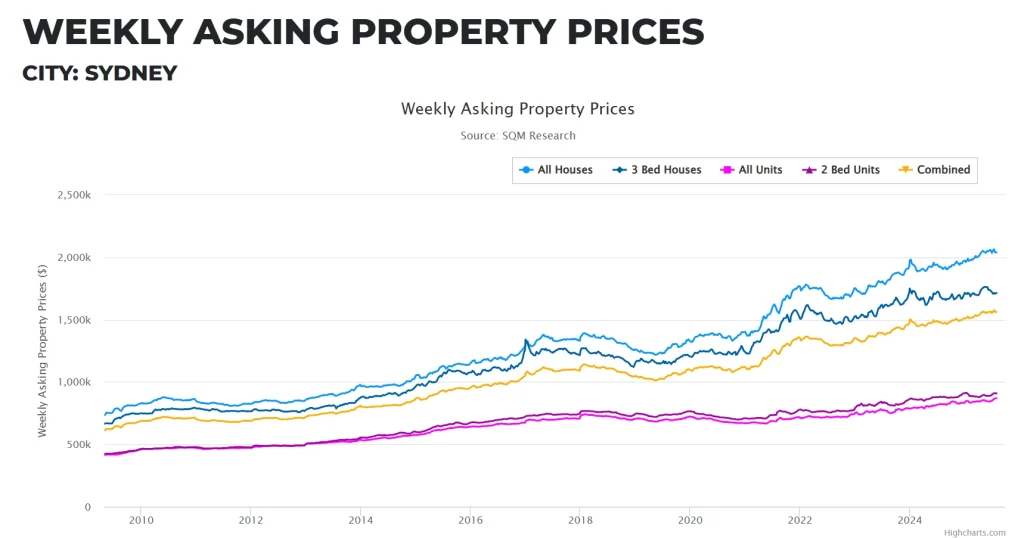

source from sqmresearch.com.au

Over the past two decades, Australia’s property market has experienced phenomenal growth. Especially in major cities such as Sydney, Melbourne and Brisbane, housing prices have repeatedly hit new highs, with an average annual growth rate of more than 6% in the past 10 years, attracting a large number of domestic and foreign investors.

However, with rising interest rates, persistent inflationary pressure, and declining household repayment capacity, the debate over a real estate bubble has once again come to the forefront of public attention.

What has driven the rapid growth of Australia’s real estate market? Is this rapid growth sustainable? Has a property bubble already formed? This article will comprehensively analyze the Australian real estate bubble from three aspects: cause analysis, potential risks and future forecasts.

2. Analysis of the Causes Behind the Soaring Housing Prices

- Stimulus in the era of low interest rates

Since 2011, the Reserve Bank of Australia (RBA) has gradually lowered the cash rate, at one point reaching a historic low of 0.1%. Long-term low interest rates have greatly stimulated demand for home purchases and investments, making real estate a “safe haven” for funds.

- Limited land supply and population growth

Although Australia has a vast land area and a relatively small population, developable land in major cities is limited—especially in areas with convenient transportation and concentrated educational and medical resources—leading to a tight housing supply. At the same time, the growing immigrant population has intensified housing demand.

- Investor-Driven Growth

Real estate in Australia is not only a residential need, but also a common tool for wealth preservation. Local investors, along with overseas buyers from countries such as China and Southeast Asia, have purchased large numbers of apartments and villas, not only boosting the rental market but also fueling overall market enthusiasm.

- Policy support

For years, the government has implemented incentive policies such as the First Home Owner Grant and negative gearing, making real estate investment more attractive. These policies have objectively encouraged speculative buying, driving up prices.

3. Potential risks: Is a bubble emerging?

While housing prices are still rising, the market is showing signs of a bubble:

- Excessive household leverage

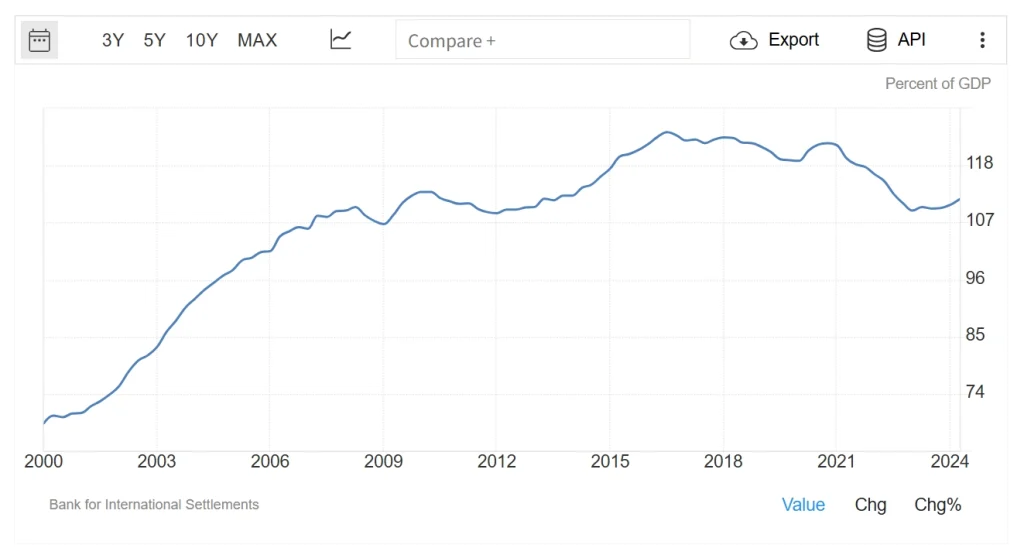

source from tradingeconomics.com/

Australia’s household debt level is among the highest in the world. In the fourth quarter of 2024, Australia’s household debt as a percentage of GDP rose to 112.10%, up from 111.50% in the third quarter. If interest rates continue to rise or the economy slows down, it will put tremendous pressure on household finances.

- Housing affordability worsens

According to the International Housing Affordability Index released by Demographia, Sydney has ranked among the top five “least affordable cities in the world” for several consecutive years. In 2023, it placed third—with a price-to-income ratio of 13.3—behind only Hong Kong (18.8) and Vancouver (13.3). The price of an average home often requires more than a decade’s worth of a household’s income to afford, significantly impacting residents’ quality of life.

- The market shows downward signals

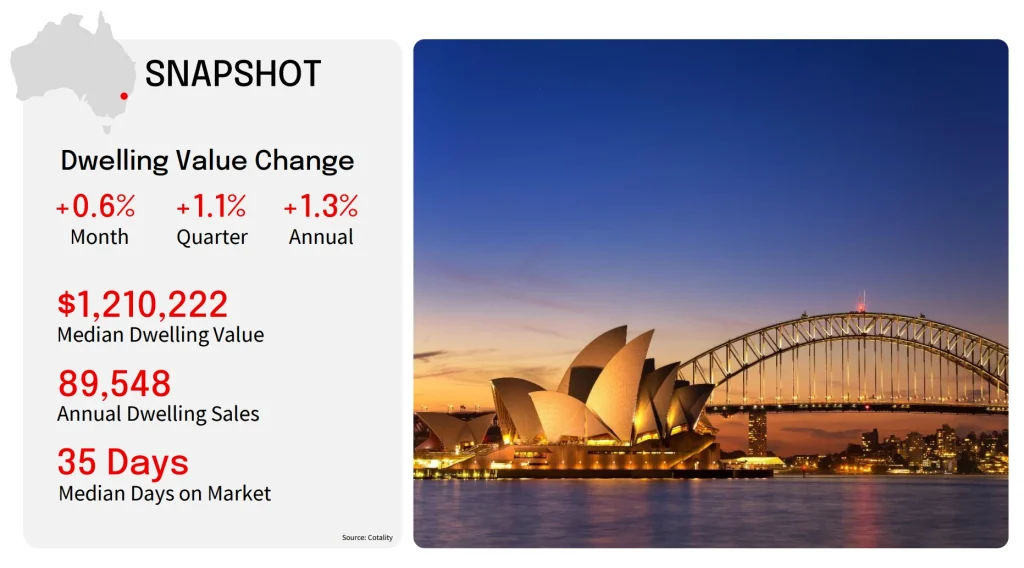

According to a Reuters report, Sydney’s residential property prices in 2025 increased by only about 3.5% year-on-year, significantly lower than the 10-year average growth rate of 6.6%.

Sydney’s sales activity continued to moderate in June, with dwelling sales volumes down 9.9% compared to the same month last year and 7.3% below the previous five-year average. House sales declined by 6.7% year-on-year, while unit sales saw a sharper drop of 13.2%.

Total listing volumes rose slightly year-on-year, with house listings increasing by 3.6% and unit listings up by 0.9% over the 12 months to June 2025. These are all signs of a “loosening bubble.”

- The interest rate reversal cycle has begun

Since mid-2023, the RBA has gradually raised interest rates, reaching 4.35% by 2025. This shift has significantly increased mortgage costs, placing heavy pressure on many homebuyers, and has also led to a slight rise in mortgage default rates among banks.

4. Future forecast: soft landing or drastic adjustment?

In the face of various risks, the future trajectory of Australia’s real estate market has attracted widespread attention. Currently, there are three main viewpoints within the industry:

- Housing prices will adjust moderately, achieving a “soft landing”

Some economists believe that although the real estate market shows signs of a bubble, the government and the central bank have a high degree of policy flexibility. Australia’s economic fundamentals remain stable, and housing demand is still strong. Therefore, housing prices are unlikely to “crash,” but instead will enter a period of short-term stagnation or slight correction, eventually achieving a “soft landing.”

- Regional differentiation

House prices in core cities such as Sydney and Melbourne remain relatively high due to high population density, concentrated employment opportunities and well-developed infrastructure. Even amid an overall market slowdown, housing prices in these cities have shown strong resilience, particularly in areas with abundant educational and healthcare resources or those located near major transportation hubs.

In contrast, inland areas or resource-based cities (such as Darwin and Perth) are more susceptible to macroeconomic fluctuations and policy changes due to their single-industry structures, high population mobility, and heavy dependence on the external economy. As a result, their housing prices may undergo more significant adjustments.

- The bubble has formed and faces systemic risks

Another group of experts pointed out that the combination of problems such as excessive market leverage, lagging income growth, and continued rising interest rates has put the real estate market in a high-risk zone. If an external shock occurs (such as global financial turmoil or a real estate credit crisis), housing prices may fall by more than 20%, and may even trigger a chain reaction such as the bankruptcy of small and medium-sized developers and an increase in bank non-performing loans.

5. How should homebuyers and investors respond?

- Buyers with urgent needs should carefully assess their own financial situation, evaluate the timing of their purchase rationally, and avoid overleveraging.

- Investors should focus on rental returns and the long-term value of the location rather than short-term increases.

- Those with high leverage should proactively develop repayment plans to avoid defaults caused by continued interest rate increases in the future.

Australia’s real estate market has accumulated many underlying instabilities during its long-term growth. While a short-term “crash” may not be imminent, we must not underestimate the potential risks.

Related Reading